Francis Dufay has spent most of his career working in e-commerce. But as CEO of Jumia Group, Africa’s most recognised e-commerce brand, he is facing his most challenging task ever.

More than a decade after it set up shop, the online retailer Jumia is still hemorrhaging money with no timeline for profitability. In its most recent earnings report, Jumia lost $167 for every $100 it earned. While its revenue from the first six months of 2023 stood at $94.8 million, it lost $63.7 million. Although its losses have reduced compared to previous years, it’s still too high for comfort. Old claims of being the “Amazon of Africa” no longer hold much value as it struggles to stay relevant in its key markets.

“Our economics was not sustainable as they may have been,” Dufay told TechCabal, referring to Jumia’s operating model over the last ten years. “The priorities needed to change.”

Dufay has risen through the ranks at Jumia over the last decade after joining the company from McKinsey, the global consulting firm. Before being named CEO in November 2022, he oversaw Jumia’s business in nine countries while reporting to former co-CEOs Jeremy Hodara and Sacha Poignonnec. Both executives resigned late last year, walking away with severance packages worth $850,000 each, according to Jumia’s financial report.

“Today, I’m managing 11 countries [and] I get to deal with a few more topics now, but it [my promotion] was not groundbreaking [or] a major transformation of my role because I was already overseeing the majority of the business at Jumia,” Dufay said. “So that helped me to make a relatively smooth transition and quickly get into the role. And I was able to make the right decisions extremely fast.”

As chief executive, Dufay inherited a struggling business that is no longer growing, putting it at risk of running out of money in a little over a year. Dufay declined to speak about his predecessors’ performance and management decisions.

Jumia’s biggest challenge at the moment is cutting costs. With a liquidity position of $166.3 million per its Q2 2023 reports, Jumia’s runway is not unlimited. It has also lost nearly a third of shoppers on its platform over the last year as the business takes drastic changes to survive.

“In the past, the focus has been fully on growth, but in a very different context where funding across the world was abundant for growth companies, which enabled many companies not to worry too much about some of the aspects of the business,” Dufay shared.

Jumia benefitted from this old reality, raising over $700 million as a startup. On two occasions, it extended its runway by selling equity on the capital market as a publicly traded company. These lifelines no longer exist because of rising interest rates in the US and an unfriendly stock market. Jumia has to adjust to this reality on its path to sustainability. “We are working hard to get the right cash utilization and cost structure so we do not need to go and beg the market for new capital,” Dufay explained.

Since his appointment, Dufay has implemented painful cuts across the company, including laying off 900 or 20% of employees. He is also reining in some profligacy, including forcing 60% of its top management team to work from the African continent instead of an office in the United Arab Emirates to save costs. The move to Africa will also remind executives of the operational realities in the markets they serve. The cuts have also hit executive compensation, and Dufay is likely to earn much less than his predecessors, according to the company’s annual report.

In 2021, former co-CEOs Hodara and Poignonnec each collected annual base salaries of nearly $480,000 and stock option incentives worth $4 million each. However, the new CEO’s base compensation is lower, hovering around $350,000 according to his annualized pay from December 2022. At least two of Jumia’s non-executive board members have also waived all or part of their hefty compensation packages in the last two years to help the company conserve cash. Last year, the company’s board members collectively earned $1.5 million in cash and stock compensation despite the company’s staggering losses.

“Of course, I’m interested in my salary,” Dufay told TechCabal about his compensation. “What matters to me is that we get back on track on growth.”

Promising early days

Launched in 2012, Jumia started operations on the continent from Nigeria as the West African country’s economy was on the verge of a restart. Government reforms from a decade earlier laid the groundwork for economic growth. As commodities prices, such as crude oil, soared during the Arab Spring, international economists expected an economic boom to usher in a new and larger middle class in Nigeria and across the continent. Nigeria, Jumia’s single biggest market today, was poised to benefit significantly from the new prosperity.

Thanks to a fast-growing population and deepening broadband connectivity, the country’s consumer internet market grew even before the first 4G internet services rolled out in 2016. McKinsey predicted these upward economic trends would widen the middle-class population to 35 million by 2030. The phrase “Africa Rising” captured this optimism while skeptics, like Standard Bank, who questioned the lofty projections about a middle-class expansion, were ignored.

Startup investors wanted to get in on the coming prosperity. Tiger Global made its entry, backing Jobberman and IrokoTV. Other investors wanted someone to guide them as they explored the unfamiliar Nigerian market. Along came the Samwer brothers, founders of Rocket Internet, a German venture studio that copied proven American business models and applied them in other markets. Rocket Internet hired the team of co-founders that built Jumia ‘s retail operations, while the Samwer trio attracted major financiers who drooled at the digital economy possibilities in the region.

Jumia took off but so did Konga, an e-commerce rival that raised over $100 million during its heyday. Jumia operated as a group of separate businesses — retail, ride-hailing, food delivery, travel booking — before consolidating in 2016. This was the early days of “startup mania” in Nigeria, and e-commerce was all the rage.

Konga and Jumia went to war, blowing millions of dollars on hiring and marketing, including promos and discounts that helped Transsion’s Tecno and Infinix smartphones grow faster. Konga folded first. It unceremoniously sold for almost nothing in 2018. Jumia remained as Nigeria grew to become its biggest market —shoppers now account for a third of all items the retailer sells.

With its triumph, the startup was listed on the New York Stock Exchange (NYSE). Jumia had successfully completed the startup lifecycle: from ideation, MVP, venture funding, product-market fit (?), scale, and finally, maturity via a stock market exit.

The struggle begins

But life as a public company has exposed the weaknesses in Jumia’s model. The firm is still a cash-burning entity that’s unable to sell a single product without losing money. Jumia’s problem is threefold.

First, the architecture for e-commerce — addressing systems, security, and fulfillment — within Africa remains fragmented a decade after Jumia launched. Historically, this has made it challenging to ship products from manufacturers and other retailers to the final consumer. This is not a new problem, but not something that Jumia can solve alone, Dufay said. Also, the proportion of households in these markets with medium and low income puts pressure on the platform to lower the prices of goods sold.

Second, economic growth in Jumia’s key market, Nigeria, slowed after 2015, and an unstable currency exchange system has cut deep into the health of several businesses. Under the Buhari government, the West African country squandered gains built over the previous decade. Excluding banks, every sector of the economy has suffered a depression. The middle class has primarily shrunk, and earlier growth projections have disappeared as inflation and devaluation put pressure on household incomes and a new wave of brain drain accelerates.

This problem isn’t unique to Jumia. Multiple companies launched in Nigeria between 2005 and 2012 have struggled after 2015. Etisalat Nigeria, the local subsidiary of the Emirati telecom company, fell apart after its dollar debt became unsustainable. South African retailer Shoprite quit the Nigerian market in 2021, 16 years after opening its first store. And in recent years, the contagion has spread, with several consumer goods companies, including those that sell on Jumia, reporting severe distress and scaling back their domestic operations. Jumia’s Dufay said Jumia Group lost $38 million in the second quarter–approximately $13 million of this loss was due to the Naira devaluation in June 2023.

But Jumia’s third problem is entirely its fault. The company played the valuation game. Rocket Internet cashed out early, leaving later-stage investors holding an overvalued company. While Jumia couldn’t do much about the economic disarray in its key markets, its operating model only worsened things.

The online retailer is available in nearly a dozen markets. But there is no good reason why. To sweeten its valuation and sell the “Amazon of Africa” narrative, it needed to show “geographical scale” — that it could operate in multiple countries even when there was no clear value proposition.

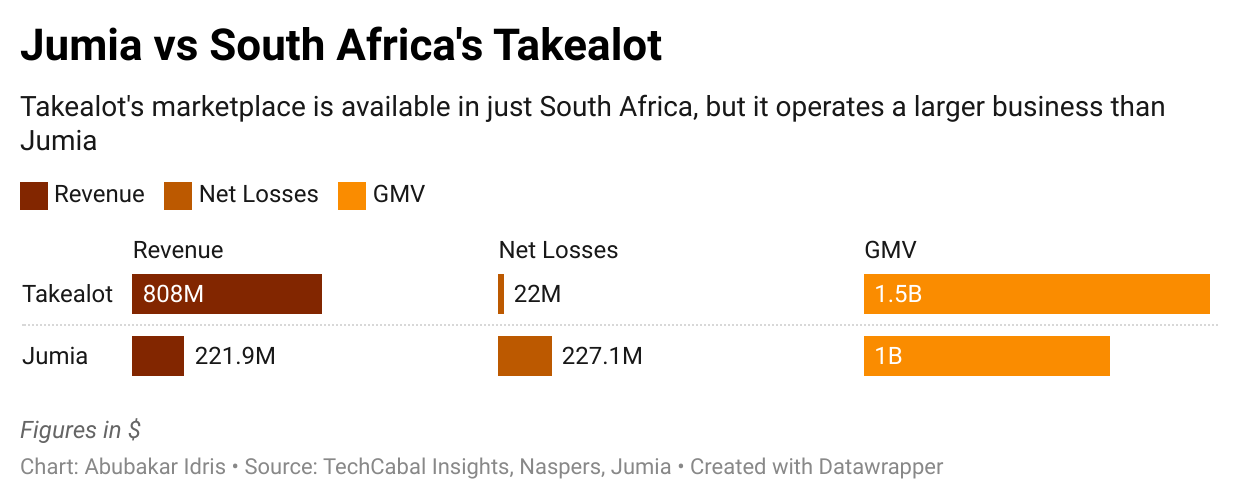

Jumia’s South African rival, Takealot, is a much smaller business by geographical spread. It operates in just that country. But its annual revenue of $808 million is nearly four times larger than Jumia’s $221.9 million. Takealot sold $1.5 billion worth of items last year; the Amazon of Africa only grossed $1.05 billion. The South African retailer is healthier, reporting losses of just $22 million, more than ten times smaller than its pan-African peer.

So when Jumia touched the coveted $1 billion valuation in early 2016, it was an outlier compared to its digital economy peers. Konga, its closest rival, was worth just $35 million then. Payments company Interswitch was worth roughly $160 million from a previous equity deal. And MainOne, whose infrastructure launched in 2010 and was pivotal to the broadband boom, didn’t even notch more than $300 million. Tiger Global’s bets — Jobberman and IrokoTV — and other startups were quite far from the unicorn mark too.

Today, Jumia is no longer a billion-dollar company. Its share price trades below $3 at the time of this report, bringing its market value to just under $270 million after Wall Street chopped it down to size.

“In Africa, anyone can build a business at burning billions,” Dufay believes. “But building a real sustainable business that adds value for customers, shareholders and employees across Africa in a new sector like e-commerce is a challenge. And I think it’s much more challenging and interesting to do that in the current context.”

Jumia’s biggest challenge in the short term is cutting costs, said Dufay, whose leadership is packed with former management consultants. This starts with shrinking the retailer’s bloated workforce expenses and management costs.

Jumia now spends over $130 million annually on its workforce and offices, more than half its total revenue. But it has costs, including deliveries ($100 million), marketing ($76 million), and technology expenses ($55 million). Throw all that in and it’s no surprise the retailer’s net losses stood at $227 million last year.

Jumia’s high workforce expenses partly stem from its complicated corporate structure. While it is active in 11 markets, its 4,318 employees as of December 2022 are scattered across 17 countries. Its headquarters is in Germany, where it sells nothing. Senior management also worked out of Dubai, UAE.

Its technology and data team is based in Porto, Portugal, because Jumia’s former co-CEOs, ex-McKinsey consultants, worried the continent lacked quality developer talent.

Jumia’s reformation begins

So far, Dufay’s changes seem to be working. Jumia’s operating losses are down 60% this year, especially advertising spend, which declined 71.7%, compared to 2022. But revenue has also dipped and the platform has lost 1 million shoppers in the last twelve months.

To bring costs to a bearable minimum, Jumia would need to close shop or limit its operations in certain geographies to classifieds rather than full-service e-commerce. Of course, this would hurt its narrative, but it’s the right thing to do.

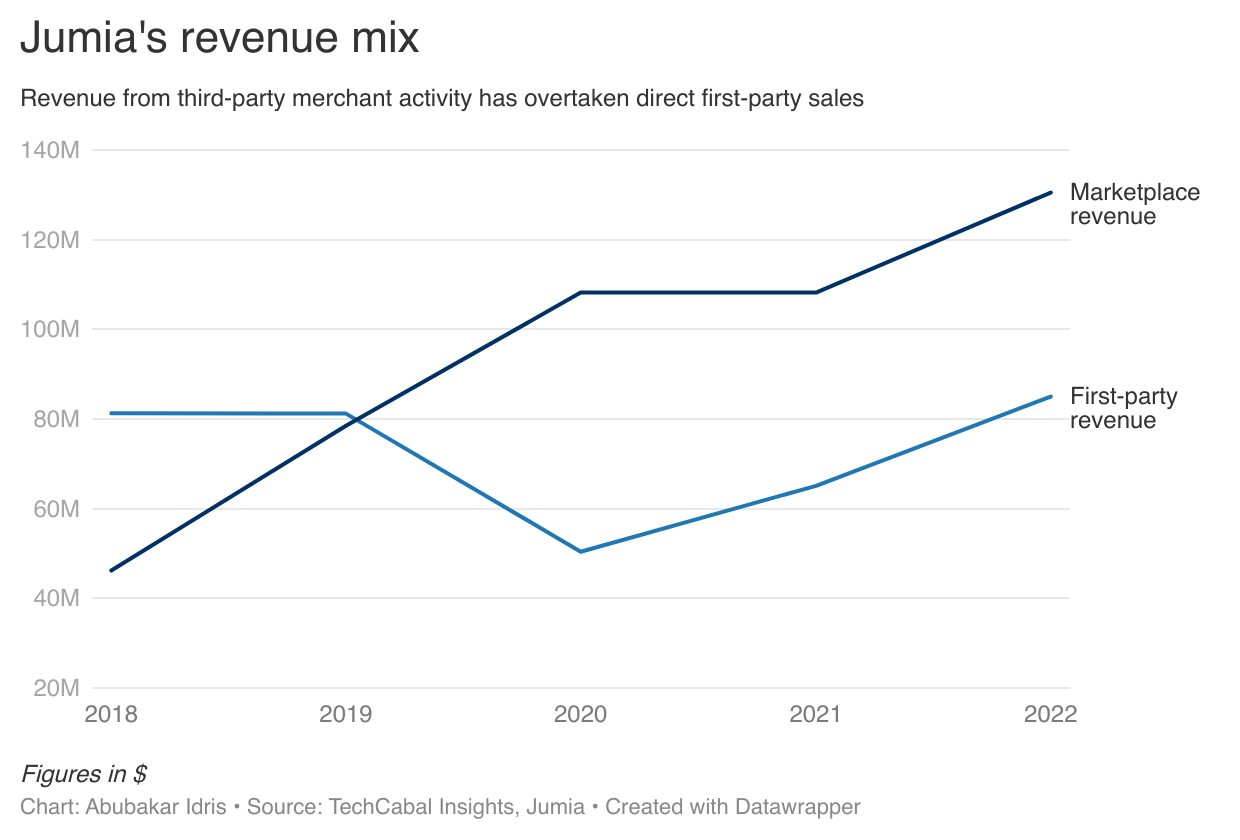

After containing costs, Dufay’s focus should shift to platform growth, especially in Nigeria and Egypt. A few years ago, Jumia successfully increased the percentage of sales from third-party merchants — marketplace revenue. At the end of last year, 61% of its revenue came from third-party vendors, saving the company the hassle of managing inventory. Instead, it operates warehouses and deliveries for a price and also earns a commission for every successful third-party sale.

High platform activity also improves network effects and potential revenue. For example, Jumia gets 1 billion page views annually. It sells advertising to external companies looking to reach people and third-party sellers to attract more buyers to the Jumia stores. Last year, marketplace ads brought in revenue of $18 million, up 67% from the previous year.

If the platform only sold its own inventory, its advertising income would have been much less. Jumia’s goal should be to re-emphasize to online vendors and customers that its platform is still the best way to shop on the domestic internet.

This would involve significant marketing and awareness campaigns to shrug off its nasty reputation for inefficiency and poor quality control. From my previous conversations with Jumia executives, they seem to underestimate the outsized impact of this negative brand perception.

However, Jumia has an advantage in the medium and long term. E-commerce is not going away, and few companies in the last decade are influential enough to boast $130 million in markets like Nigeria and Egypt.

“The demand is there and it’s up to us to serve the demand; so we’re coming back to life we building the right fundamentals,” Dufay explained. “What people need to be aware of is that this company is coming back.”

Editor’s note: This article has been corrected to reflect Jumia’s liquidity position as $166.3 million and to show that the amount lost to Naira devaluation was $13 million.

Have you got your tickets to TechCabal’s Moonshot Conference? Click here to do so now!

Get the best African tech newsletters in your inbox

>>> Read full article>>>

Copyright for syndicated content belongs to the linked Source : TechCabal – https://techcabal.com/2023/09/21/exclusive-inside-francis-dufays-urgent-plans-to-rescue-jumia-the-struggling-amazon-of-africa/

{kind=link}