Vendor consolidation is real. Senior IT executives share their input from the buyer’s perspective.

As the tech economy has adjusted to the current economic environment, there has been a great deal of debate in both the vendor and investor communities about vendor consolidation. While there is little doubt that companies have been cutting back on expenses generally in response to economic uncertainty, startups in particular have been feeling the pain of contracting budgets and reluctant investors.

Thanks to the team at Foundry, I was able to gain input from those whose opinions matter most – the senior IT executives at mid-sized to large companies who are placing the purchase orders and determining which vendors to leverage – and which to cut back. We recently ran a poll on the CIO Tech Talk community to ask questions and gauge input on the topic of vendor consolidation from the buyer’s perspective: how real it is, how widespread, and whether this is a permanent shift or just a short-term blip.

Our poll received excellent feedback – in addition to receiving a significant base of survey respondents, a number of community members provided additional commentary. While I expected this exercise to confirm that consolidation is real, I was pleasantly surprised with the degree to which the CIO Tech Talk Community confirmed it – and how they are taking steps to realign their procurement and vendor management strategies.

Vendor consolidation is very real

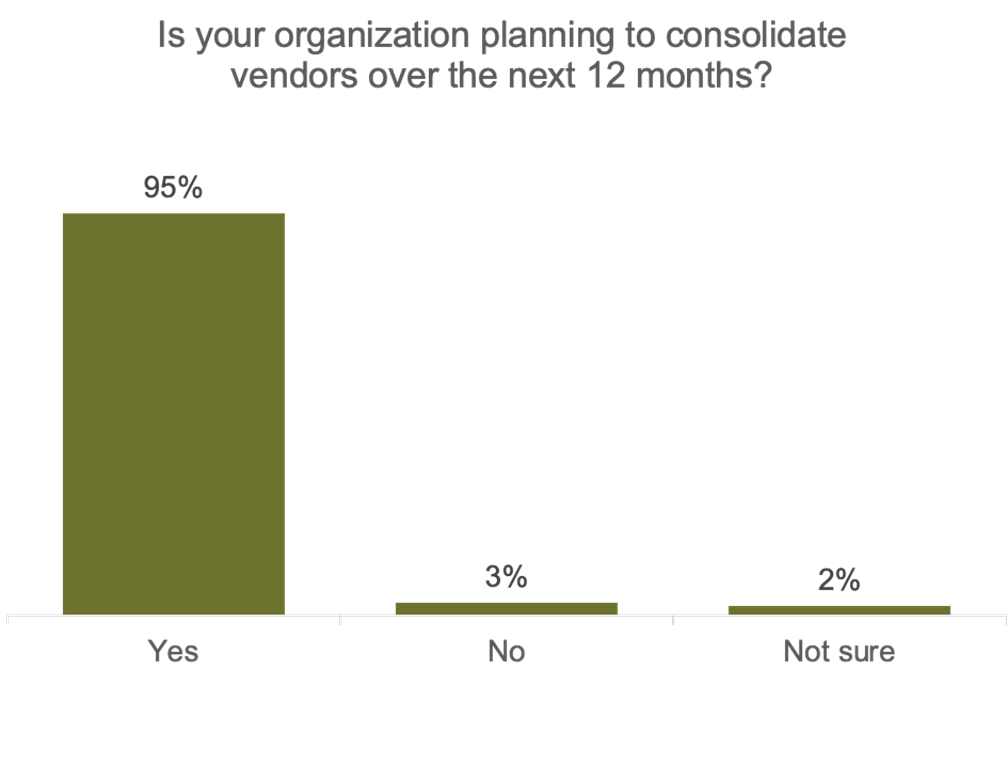

We got right to the point with the first question – “Is your organization planning to consolidate vendors in the next 12 months” – and the answer we got back from the community was stunningly clear and unambiguous – 95% of respondents confirmed that, yes, they are planning to consolidate.

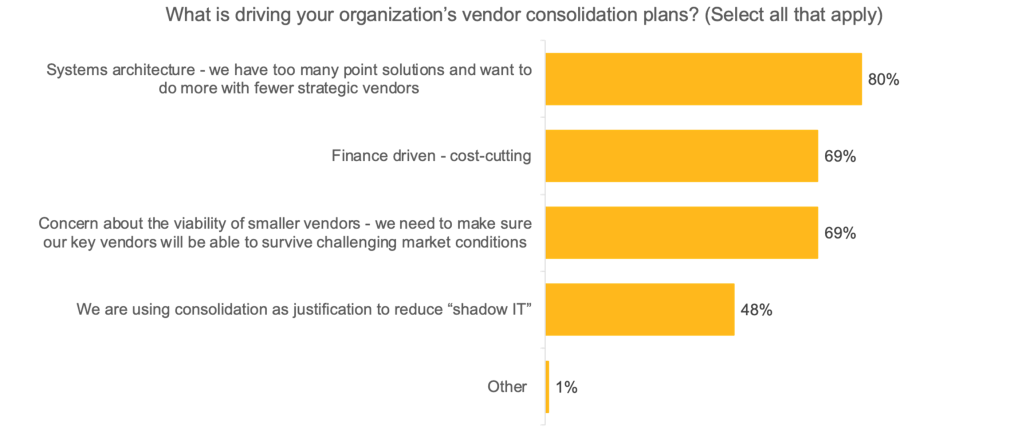

When we asked what’s driving that consolidation, finance-driven reasons were close to – but not at – the top. An even greater reason given was the desire to consolidate systems architecture and reduce the number of “point solutions” – which 80% of respondents cited as a consolidation driver – while 69% of respondents cited finance driven cost-cutting.

As buyers consolidate, pressure on vendors increases

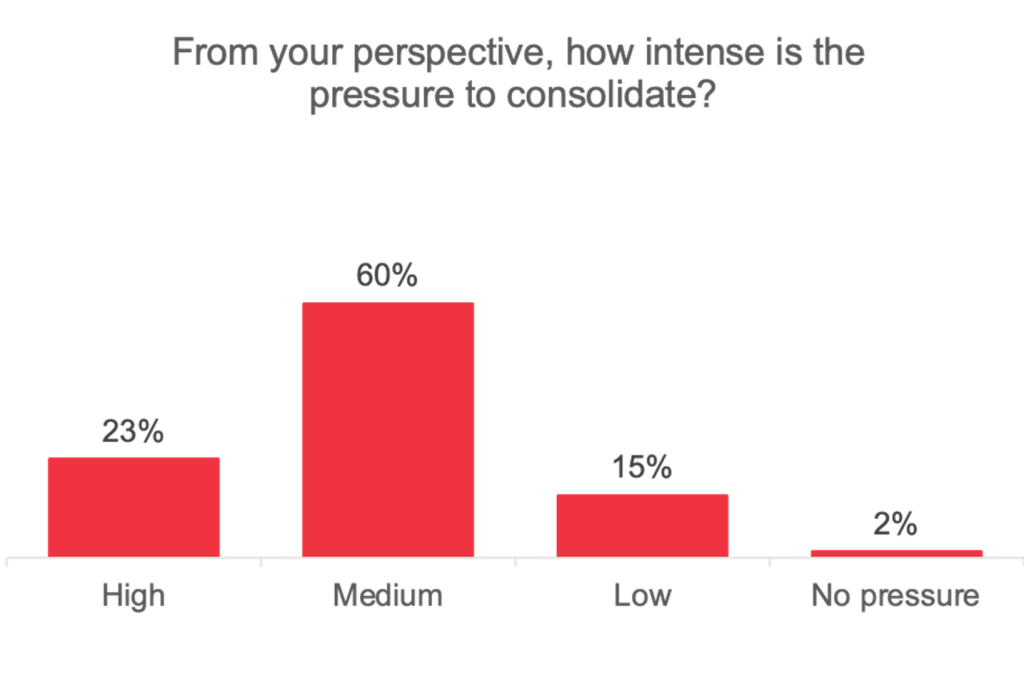

Clearly there is pressure to consolidate – both internally and externally driven. When we asked about the intensity of that pressure, 83% cited a moderate to high degree of pressure.

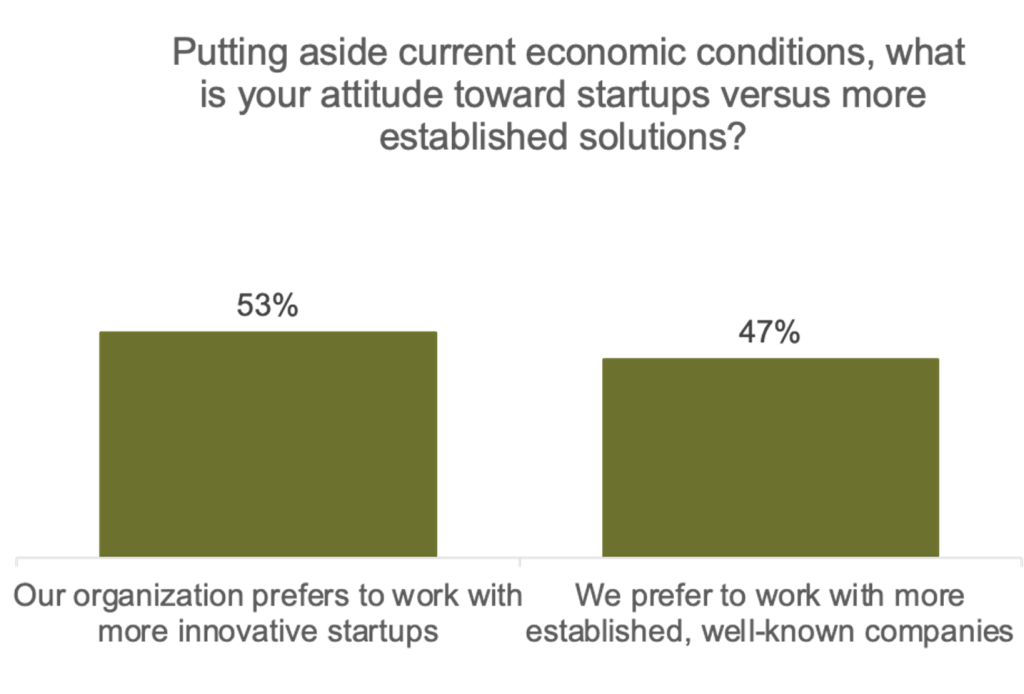

The implications are clear – IT organizations and environments have both reasons and motivations for reducing the number of vendors they are working with – and while the survey respondents were more evenly split on whether they prefer to work with smaller, more innovative vendors, vs larger, more established ones, I’d suggest that it’s highly likely that the smaller vendors will be the most impacted. By definition, of course, the larger vendors offer a greater degree of capability – if organizations are reducing the number of vendors they choose to work with, it only makes sense to focus on eliminating those with the smaller functional footprints, even if there is some degree of preference for innovation.

10X in 10 Years – can this continue?

Vendors continue to proliferate – for instance, venture capitalist Matt Turck of Firstmark Capital has been building an annual “landscape” of Machine Learning, Artificial Intelligence and Data (“MAD”) offerings since 2012, and the number of vendors has increased from 139 in 2012 to 1,416 in 2023. At this point in time, it needs to be asked whether such a rapid increase in the number of vendors is sustainable. Based on the feedback from the CIO Tech Talk base, at least for the near-term the answer appears to be “no”.

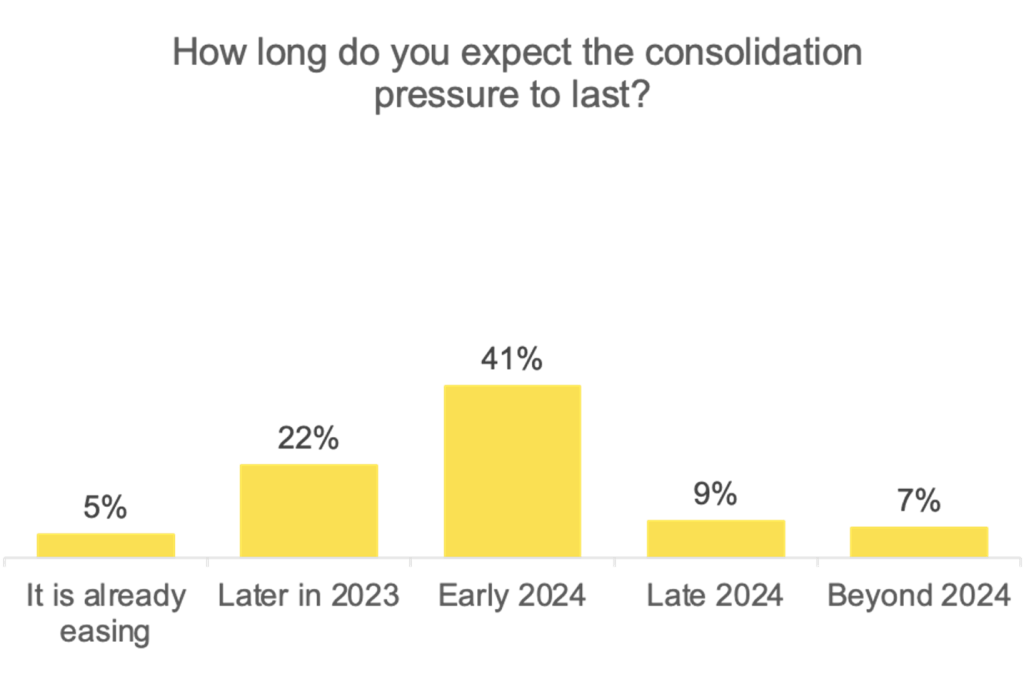

When we asked the survey respondents how long they expect consolidation pressure to last, the result was a more normal distribution centered around early/mid 2024 – but with a significant number of them expecting that this pressure will be ongoing.

Consolidation has benefits – for buyers at least

The commentary on the poll was extensive – Tech Talk Community members had a great deal to say about this topic, and their commentary is illuminating. It’s quite clear that many buyers see consolidation as a good thing – even if vendors and venture capitalists are obviously less sanguine.

Among the stated benefits from a buyer’s perspective:

Price/cost reduction

“By consolidating vendors, our company can negotiate better pricing terms and volume discounts since we have higher purchasing power”

“Consolidating vendors can reduce costs by centralizing purchasing, simplifying contract management, and minimizing administrative efforts”

Efficiency

“By working with fewer vendors, we can save time and resources on communication, negotiation, and admin tasks”

“Efficiency by streamlining procurement processes and reducing the complexity and variability of your supply chain”

“Vendor consolidation is a good way to manage the resources”

“Vendor consolidation can lead to greater efficiency and consistency”

Improved supply chain management

“Relying on too many vendors introduces higher risks related to quality control issues, delivery delays, or disruptions in the supply chain”

“It’s very important to enhance supply chain visibility”

“Vendor consolidation can be a great way to simplify our supply chain and reduce costs”

Economic outlook

“Economic outlook and AI lead to higher vendor consolidation.”

“The importance of AI in the industry is irreversible”

“Inflation and economy also key factors”

Sustainability

“By working with fewer vendors, we can more easily track and manage our environmental impact, and potentially negotiate better deals on sustainable materials and practices”

“I think vendor consolidation could help us improve our sustainability efforts”

Improved vendor communication/collaboration

“Vendor consolidation can lead to better communication, mutual understanding of business goals, increased trust, and ultimately more reliable service from vendors”

“With fewer vendors to manage, organizations may be able to build stronger, more collaborative relationships with their remaining vendors”

Quality of service

“It’s difficult to manage the quality of the service for the companies who have many vendors”

Other

“We consolidate vendors when we can, but in many cases, we don’t have the opportunity due to either cost or product offerings from every ISV”

There were also a few customers with concerns about consolidation

“If we rely too heavily on a single vendor and they experience problems, it could have a significant impact on our operations”

“I’m concerned that consolidating vendors could lead to a loss of diversity in our supply chain.”

“Personally, I am against consolidation, however in the company the board is also opting for consolidation of suppliers. I think it is a certain risk in the long term, because if for some reason in the future you need to change suppliers, and you have many services consolidated with them, this will be a laborious, expensive and time-consuming process.”

“Reducing the number of vendors can lead to a loss of competition, which may result in less innovation and lower quality products or services”

“Vendor consolidation might result in decreased innovation or limited choice for businesses seeking specialized solutions.”

What’s next?

I believe there are a few potential implications.

The most obvious one is a significant number of mergers and acquisitions (M&A) in the vendor community. Of course, M&A in the tech space is nothing particularly new, but barring a radical change in economic conditions, one can expect it to accelerate dramatically over the next 12-24 months as many venture-backed companies run perilously low on funds, and venture capital providers triage their portfolios to preserve funds for the most likely survivors. Private equity has played and will continue to play an important role in this consolidation, as a Synergy Research poll earlier this year strongly indicated, with private equity accounting for 91% of closed M&A deals in the past year.

Of course, some startups will also shutdown. According to recent data from Carta, Q3 2023 saw the highest number of startup shutdowns yet due to bankruptcy or dissolution.

Another longer-term implication is the degree to which organizations are gravitating toward vertically-oriented, business-specific applications vs. more general-purpose horizontal platforms. By definition, any vertical solution will have fewer alternatives, a broader functional footprint and are less likely candidates for consolidation – for instance in a manufacturing company, manufacturing-specific applications are going to be less likely to be consolidated than horizontal IT platforms. I’ll be discussing vertical vs horizontal solutions and their respective defensibility in a future post.

Of course, what most industry participants are hoping for is ongoing economic recovery. I do expect the economy to continue improving – despite the turmoil currently in the world driven by the conflicts in Eastern Europe and the Middle East – and the possibility of new conflict in Asia and elsewhere, election years tend to be good for the economy overall. Also the recent moderation of inflation, and IPOs of companies such as Klaviyo, Instacart & Arm, are hopeful signs that financial markets are starting to at least somewhat normalize.

However economic recovery does not imply that financial markets will return to creating as many startups as we have seen in recent years. I expect – and CIO Tech Talk readers clearly seem to agree – that the “new normal” will consist of fewer, financially stronger vendors.

SUBSCRIBE TO OUR NEWSLETTER

From our editors straight to your inbox

Get started by entering your email address below.

Please enter a valid email address

>>> Read full article>>>

Copyright for syndicated content belongs to the linked Source : CIO – https://www.cio.com/article/657327/what-it-executives-are-saying-about-vendor-consolidation.html

{kind=link}