Home Fossil Energy Interview: With new oil & gas horizons calling, will the North Sea hold sway over its existing rig fleet?

This is a free premium article to give you a sample of what Offshore Energy has to offer as part of our premium section. You can upgrade to premium access here.

Illustration; Source: MSI

Illustration; Source: MSI

As the ongoing drilling upcycle empowers rig owners, new offshore drilling playgrounds with better benefits are popping up on the companies’ radars. This interview sheds more light on whether this trend will lead to a further exodus from the North Sea market and a mass pivot toward other destinations.

While emission reduction quests are part of the long-term energy transition game, the short-term outlook does not foresee a wave of new rig upgrades to curb the carbon footprint due to the current market fundamentals, according to Todd Jensen, Senior Offshore Energy Market Analyst at Maritime Strategies International (MSI), a UK-headquartered provider of market forecasting and business advisory services for shipping, offshore and allied industries.

The latest analysis of the North Sea drilling scene, recently compiled by MSI, which is focused on the mobile offshore drilling unit (MODU) market spotlights the rig owners’ growing opportunities to play the options while lucrative alternatives continue to keep the North Sea MODU market tight. The regional tonnage demand is set to get a boost in 2024, driving day rates further upward against a limited fleet supply picture.

Maritime Strategies International predicts the North Sea MODU demand to rise as the current upcycle continues to run its course with demand for jack-ups and floaters forecast to increase between 2023 and 2024 by 30% and 39%, respectively. As MSI’s forecast indicates post-2024 rig demand will experience a downward trajectory while remaining high, this trend slightly differs from other regions where demand is estimated to peak in 2026 or 2027.

Courtesy of MSI

Courtesy of MSI

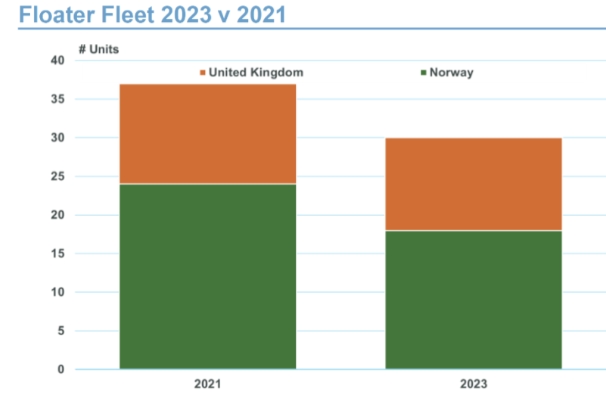

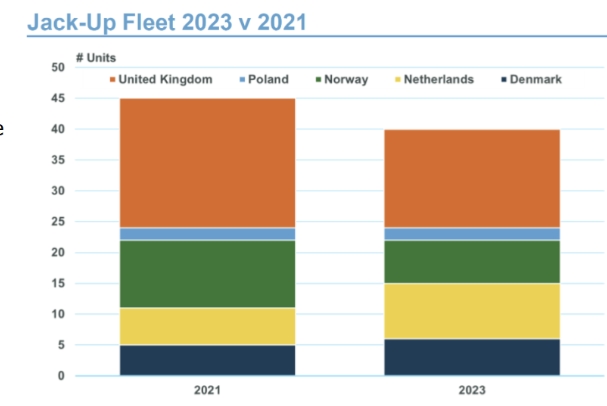

It is no secret that the North Sea MODU fleet has been struggling to remain in the region in the face of more lucrative international deals available to rig contractors. MSI underlines that this is driving more MODUs to leave the North Sea for longer-term contracts. The hurdles operators and rig owners have been experiencing are further compounded by the UK government’s windfall tax and uncertain rules towards the oil and gas sector.

MSI claims that high demand for MODUs will continue until the latter stages of the decade. However, the risk is still present that further floaters could leave the North Sea to regions such as West Africa and South America while more jack-ups could head to Asia and West Africa since the North Sea typically sees lower day rates and shorter-term contracts than elsewhere due to its strong historical activity rates and previously abundant supply of MODUs.

MSI outlines that utilization is still high within the region with only seven jack-ups and nine floaters not currently active. Looking into current North Sea contract activity shows many positive signs, thanks to several contract extensions and new deals, which were signed during 4Q 2023, including deals involving the reactivation of units.

Source: MSI

Source: MSI

In line with this, Dolphin Drilling’s deal with EnQuest will see the Borgland Dolphin semi-submersible reactivated for a contract with an initial period of 137 days but with options to extend up to nearly five years. In addition, Equinor also acted to secure MODU supply, agreeing to pay a higher day rate to retain Odfjell Drilling’s Deepsea Aberdeen semi-sub. The new rate is $450,000/day and confirms the use of the unit until 4Q 2025.

Moreover, MSI points out that NW Europe is more advanced in the energy transition journey than many regions with offshore wind being a key part of this. As countries progress further in the energy transformation game, demand for MODUs is anticipated to decrease as less oil and gas drilling is carried out.

As a result, Maritime Strategies International expects to see some aspects of the energy transition engine requiring MODUs in the long term, such as carbon capture and storage (CCS) and decommissioning of oil and gas fields.

As the energy transition gathers pace, plug and abandonment work is expected to play a significant part in future North Sea MODU demand with decommissioning within the North Sea said to be worth $20 billion in the long term.

video

Posted: 2 months ago

MSI uses two recent contracts to illustrate the use of MODUs in the CCS sector. One of these is the deal that TAQA awarded to the Valaris 123 jack-up rig to drill wells on the Porthos CCS project in the Dutch North Sea, expected to begin in late 2024. In addition, two contracts have been handed out to the Valaris 72 and Valaris 292 jack-ups for the Hynet CCS project in the East Irish Sea, with the planned workload, said to be ‘substantial.’

On the other hand, Diamond Offshore, which has four MODUs in the North Sea, also witnessed a keen interest in retaining units, as it confirmed deals for the Ocean GreatWhite and Ocean Patriot semi-sub rigs. While BP has opted to exercise the second and third extensions for the Ocean GreatWhite, keeping it busy until August 2024, TAQA Bratani has signed the Ocean Patriot for a 35-well plug and abandonment project, representing three years of firm work due to start in 2025.

More drilling work but less decarbonization revamps on rigs’ agendas

Aiming to glean more insight into the offshore drilling market trends not just in the North Sea but also globally, Offshore Energy had an interview with Todd Jensen, MSI’s Senior Offshore Energy Market Analyst, regarding the existing North Sea challenges for MODUs and possible pathways to retain these rigs in the region. Bearing in mind the energy transition’s role in mitigating climate change, potential rig upgrades, which would enable emission cuts and bring fresh impetus to up the decarbonization ante during offshore drilling operations, were also discussed.

Jensen, who holds an MSci in Geology from the University of Southampton, was a perfect candidate to delve into these subjects as he leads MSI’s offshore energy market analysis with a focus on oil and gas field development projects, alongside offshore renewables. Aside from being in charge of the maintenance and development of MSI’s proprietary offshore energy databases and sector models, Jensen contributes to market reports and consultancy projects.

Before joining MSI, he worked as a Research Analyst for energy market intelligence companies Westwood Global Energy Group and Wood Mackenzie, covering upstream oil and gas and related oilfield services. Let us take you along for the ride during this interview, as Jensen offers his take on the pressing issues in the MODU market and dives into the ins and outs of the current and future offshore drilling landscape.

Q: Since the North Sea is a mature basin, production is forecasted to decline over the years, but we still see new oil and gas discoveries popping up now and then, bringing fresh untapped reserves in the spotlight that could be developed. Do you foresee further hydrocarbon exploration in the North Sea beyond 2030?

Todd Jensen: I think there is a possibility we will see exploration drilling in the North Sea beyond 2030. On January 30, 2024, the UK announced the award of 24 licenses in the UK North Sea to a group of 17 companies. As well as the usual majors, there was also a good amount of interest from independent oil and gas operators.

With companies showing an appetite to explore the North Sea, we are likely to see exploration continue into the 2030s, albeit to a lesser extent than we have seen in the past as companies continue to be more reserved with capex.

Q: Should rig owners anticipate a further rise in day rates and fleet utilization for jack-ups and floaters over the next few years?

Todd Jensen: MSI anticipates day rates to keep increasing until 2026, however, rigs are already being contracted for 2025 and into 2026, so we are seeing those contracts being signed now. Utilization for both jack-ups and floaters is expected to increase in 2024 and 2025. Jack-up utilization is expected to decline from 2026 and beyond with a few newbuilds expected to enter the market.

Floaters are also expected to see peak utilization in 2026 with key projects in West Africa and South America lined up for 2024 and 2025. However, there is less scope for newbuild floating rigs with newbuild prices exceeding $500 million deterring investment in a historically volatile market.

Based on MSI’s recent forecast, the demand for MODUSs will be steadily reduced post-2024, however, it is still predicted to remain high. While the MODU market continues to tighten, how can North Sea operators keep these rigs from leaving the region for greener postures?

Todd Jensen: We have already seen some response to this with floating rigs being tied into contract extensions or longer contracts. If rig owners can be sure of longer-term work they will be less likely to leave. The North Sea will likely see day rates naturally increase in line with the global market, but I believe it is the longevity of the contracts that owners are after.

Q: With energy transition making inroads, especially in the North Sea, do you anticipate more rig upgrades to curb emissions from operations?

Todd Jensen: In the short term no, rig utilization at the moment is strong and no one will want to remove a rig from service to upgrade it. Once the current upcycle starts to tail off, we will likely see some of the older jack-up and floating rigs being scrapped as demand decreases; newer, more efficient rigs will then become more favorable.

Q: As the decommissioning of depleted fields is on the rise, what kind of idle MODUs do you believe can be quickly refurbished for such work? Which type of MODU would be best suited for CCS work and how can existing rigs be revamped for such activities?

Todd Jensen: Decommissioning requires in-fill drilling which is largely carried out by the same rigs that drill the wells. In-fill drilling can utilize lower-powered rigs due to the fact they do not have to drill the original hole. As seen over the last couple of years, rig owners are not reactivating floaters unless they have a contract in place, therefore, I do not see rigs being reactivated specifically for decommissioning work.

Drilling for CCS will also struggle to compete with the oil and gas industry in the short term, with some CCS projects simply being priced out of the equation due to the day rates rigs are achieving in the oil and gas industry.

Q: Do you anticipate more rig conversions for offshore wind installation work? Will these conversions be a more profitable undertaking for developers and the supply chain rather than newbuild vessels? What are the pros and cons of such conversions?

Todd Jensen: In the current market, MODU owners will achieve greater day rates from drilling for oil and gas, so I do not see many rig owners being interested in conversions right now. Conversion of a drillship into a WTIV would cost in the region of $100-200 million, so is by no means, a light undertaking, despite being half the price of a newbuild WTIV.

The pros are a shorter duration required to get the vessel into the wind market and the cost is cheaper than newbuilds. Cons include the fact MODUs are not designed for turbine installation and lack the stability and deck space required to install larger wind turbines.

![]()

ADVERTISE ON OFFSHORE ENERGY

𝐃𝐨 𝐲𝐨𝐮 𝐰𝐚𝐧𝐭 𝐭𝐨 𝐠𝐫𝐚𝐛 𝐭𝐡𝐞 𝐚𝐭𝐭𝐞𝐧𝐭𝐢𝐨𝐧 𝐨𝐟 𝐲𝐨𝐮𝐫 𝐭𝐚𝐫𝐠𝐞𝐭 𝐚𝐮𝐝𝐢𝐞𝐧𝐜𝐞 𝐢𝐧 𝐨𝐧𝐞 𝐦𝐨𝐯𝐞? 𝐋𝐨𝐨𝐤 𝐧𝐨 𝐟𝐮𝐫𝐭𝐡𝐞𝐫 𝐭𝐡𝐚𝐧 𝐎𝐟𝐟𝐬𝐡𝐨𝐫𝐞 𝐄𝐧𝐞𝐫𝐠𝐲! 𝐎𝐮𝐫 𝐜𝐨𝐧𝐭𝐞𝐧𝐭 𝐢𝐬 𝐫𝐞𝐚𝐝 𝐛𝐲 𝐭𝐡𝐨𝐮𝐬𝐚𝐧𝐝𝐬 𝐨𝐟 𝐩𝐫𝐨𝐟𝐞𝐬𝐬𝐢𝐨𝐧𝐚𝐥𝐬 𝐞𝐧𝐠𝐚𝐠𝐞𝐝 𝐢𝐧 𝐨𝐢𝐥 & 𝐠𝐚𝐬, 𝐦𝐚𝐫𝐢𝐭𝐢𝐦𝐞, 𝐨𝐟𝐟𝐬𝐡𝐨𝐫𝐞 𝐰𝐢𝐧𝐝, 𝐠𝐫𝐞𝐞𝐧 𝐦𝐚𝐫𝐢𝐧𝐞, 𝐡𝐲𝐝𝐫𝐨𝐠𝐞𝐧, 𝐬𝐮𝐛𝐬𝐞𝐚, 𝐦𝐚𝐫𝐢𝐧𝐞 𝐞𝐧𝐞𝐫𝐠𝐲, 𝐚𝐥𝐭𝐞𝐫𝐧𝐚𝐭𝐢𝐯𝐞 𝐟𝐮𝐞𝐥𝐬, 𝐬𝐡𝐢𝐩𝐩𝐢𝐧𝐠, 𝐚𝐧𝐝 𝐨𝐭𝐡𝐞𝐫 𝐢𝐧𝐝𝐮𝐬𝐭𝐫𝐢𝐞𝐬 𝐨𝐧 𝐚 𝐝𝐚𝐢𝐥𝐲 𝐛𝐚𝐬𝐢𝐬.

Follow Offshore Energy’s Fossil Energy market on social media channels:

>>> Read full article>>>

Copyright for syndicated content belongs to the linked Source : OffshoreEnergy – https://www.offshore-energy.biz/interview-with-new-oil-gas-horizons-calling-will-the-north-sea-hold-sway-over-its-existing-rig-fleet/

{kind=link}